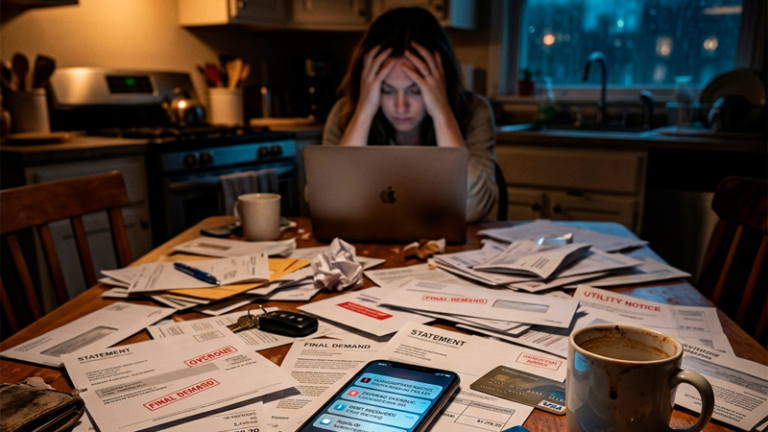

High Income Households Are Quietly Living Paycheck to Paycheck

A surprising number of people earning $150,000 to $300,000 per year still feel financially trapped.

From the outside, their lives look stable.

Nice apartment.

New SUV.

Frequent travel.

Updated phones.

Weekend dinners.

Private school payments.

Streaming subscriptions everywhere.

But behind those appearances, many higher-income households are carrying intense monthly pressure.

Large salaries create a dangerous illusion because outsiders assume income automatically equals financial security. In reality, spending often expands just as quickly as earnings rise.

Some households making six figures have less emergency savings than families earning half as much.

That contradiction has become increasingly common in expensive American cities.

Lifestyle Inflation Usually Starts Small Before Becoming Permanent

Most people do not suddenly transform their spending overnight after receiving raises.

The shift happens gradually.

Someone upgrades:

- from a used car to a leased luxury SUV

- from a starter apartment to a high-rise building

- from cooking at home to constant delivery apps

- from budget flights to premium travel habits

Each decision feels reasonable individually.

After all, earning more money should improve quality of life.

The problem appears when recurring expenses become locked into the monthly budget.

A household that once comfortably lived on $5,500 monthly expenses can slowly drift toward:

- $9,000 rent and mortgage obligations

- $1,400 car payments

- $700 dining budgets

- $1,200 childcare costs

- $900 insurance bills

At some point, the higher salary stops feeling “high.”

Instead, it becomes necessary just to maintain the current lifestyle.

The income increased, but financial flexibility quietly disappeared.

High Earners Often Normalize Expensive Financial Decisions

One overlooked problem with higher-income social circles is comparison pressure.

People naturally adjust expectations based on their environment.

If friends, coworkers, or neighbors regularly discuss:

- luxury vacations

- designer purchases

- private schools

- expensive restaurants

- home renovations

- premium gyms

those expenses slowly begin feeling normal.

Someone earning a strong salary may genuinely believe they are “doing average” financially while spending dramatically more than necessary.

This especially happens in industries where appearance influences professional perception.

Workers in fields like:

- finance

- real estate

- tech

- law

- sales

often feel subtle pressure to maintain a polished image.

That pressure creates hidden spending categories:

- luxury watches

- expensive clothing

- newer vehicles

- premium apartments near downtown areas

- networking dinners

- frequent social spending

Some high-income earners are not spending to impress strangers. They are spending to avoid feeling left behind by peers.

That emotional pressure rarely gets discussed openly.

Large Monthly Payments Quietly Eliminate Financial Freedom

A household may technically earn impressive income while still having almost no flexibility.

That usually happens when fixed obligations become too large.

For example:

- $4,200 mortgage

- $1,100 car lease

- $2,300 daycare

- $850 student loans

- $600 insurance

- $1,000 minimum credit card payments

At that point, even a strong salary can start feeling fragile.

One unexpected event suddenly creates panic:

- job loss

- medical leave

- reduced commissions

- economic slowdown

- emergency repairs

High incomes often create confidence, but oversized fixed expenses create vulnerability at the exact same time.

This explains why some professionals experience enormous stress despite earning salaries many Americans would consider wealthy.

The pressure is not always about income.

It is often about obligations.

Credit Cards Quietly Fill the Gap Between Income and Lifestyle

A common pattern among financially stressed high earners is reliance on short-term borrowing to maintain appearances.

That can include:

- credit card balances

- buy now pay later services

- personal loans

- refinancing cycles

- home equity borrowing

People often assume debt problems mainly affect low-income households.

That assumption is inaccurate.

Many six-figure earners carry:

- $15,000 to $40,000 credit card balances

- luxury auto debt

- oversized mortgages

- high-interest personal loans

Some continue spending aggressively because their income allows minimum payments to remain manageable temporarily.

But interest accumulation changes everything over time.

A person carrying $28,000 in revolving credit card debt at high interest can lose thousands annually without reducing principal meaningfully.

The paycheck may look large, but the financial drain happening underneath becomes enormous.

This creates a strange situation where someone earning excellent income still feels constant monthly stress.

Children Make Financial Pressure Multiply Faster Than Many Expect

Many professionals first notice financial strain after starting families.

Child-related costs arrive rapidly:

- daycare

- larger housing

- health insurance

- activities

- food

- transportation

- education savings

In major cities, daycare alone can exceed:

- $1,500 monthly

- sometimes even $3,000+ per child

Couples who previously felt financially comfortable suddenly discover their old lifestyle no longer fits reality.

But instead of reducing spending, many households try maintaining every previous habit simultaneously.

That means continuing:

- luxury travel

- expensive cars

- premium shopping habits

- constant dining out

- subscription overload

while adding childcare expenses on top.

This is where many higher-income households quietly start depending on every paycheck arriving exactly on schedule.

Without realizing it, they lose the margin that once made their finances feel safe.

A Smaller Lifestyle Sometimes Creates More Peace Than More Income

One interesting pattern appears repeatedly among financially stable households.

Many are not necessarily the highest earners.

Instead, they maintain:

- lower fixed expenses

- older paid-off vehicles

- moderate housing costs

- manageable lifestyles

- emergency savings buffers

Those choices create breathing room.

Someone earning $95,000 annually with controlled expenses may experience far less stress than a household earning $240,000 while drowning in obligations.

That comparison surprises many people because modern culture often focuses heavily on visible success indicators.

But visible wealth and actual financial stability are not always the same thing.

A smaller lifestyle with lower pressure often creates more long-term freedom than a larger lifestyle supported entirely by ongoing income.

That realization changes how many people define financial success.

FAQ

Can high-income households really live paycheck to paycheck?

Yes. Large salaries do not automatically create savings if spending grows equally fast. High housing costs, debt, childcare, and lifestyle inflation can consume income surprisingly quickly.

What is lifestyle inflation?

Lifestyle inflation happens when spending increases alongside income growth. As earnings rise, people gradually upgrade housing, transportation, travel, dining, and daily habits until expenses absorb most of the additional income.

Which expenses create the most pressure for high earners?

Common financial pressure points include:

- housing payments

- luxury vehicle leases

- childcare

- student loans

- credit card debt

- private education

- recurring subscriptions

Fixed monthly obligations are often the biggest issue.

How can higher-income households regain financial flexibility?

Many improve financial stability by:

- reducing recurring expenses

- downsizing vehicles

- limiting debt growth

- rebuilding emergency savings

- avoiding unnecessary luxury spending

- controlling lifestyle inflation

Financial Stress Does Not Always Match Income Levels

A lot of Americans still imagine financial struggle as something tied only to low salaries.

But modern financial pressure became more complicated than that.

In expensive cities especially, people earning impressive incomes can still feel trapped by:

- oversized monthly obligations

- debt accumulation

- social comparison

- rising living costs

- lifestyle expectations

Some eventually realize they were earning more money than ever while feeling less financially secure than before.

And for many households, the biggest improvement does not come from another raise.

It comes from finally reducing the pressure created by everything surrounding the paycheck.