Subscription Habits That Quietly Destroy Monthly Budgets

A lot of people think financial problems usually come from big purchases.

Car payments. Credit card debt. Expensive vacations. Huge medical bills.

Those things absolutely matter, but many monthly budgets start collapsing somewhere much smaller and much harder to notice. A few subscriptions here, another auto-renewal there, and suddenly hundreds of dollars disappear every month without creating much value.

What makes subscription spending dangerous is how invisible it becomes over time. People stop evaluating the cost emotionally after the second or third payment. The charge becomes background noise.

That is exactly why subscription fatigue has become one of the most overlooked money problems in the last few years.

Most People Underestimate Their Real Subscription Costs

Ask someone how much they spend monthly on subscriptions and they will usually guess low.

Very low.

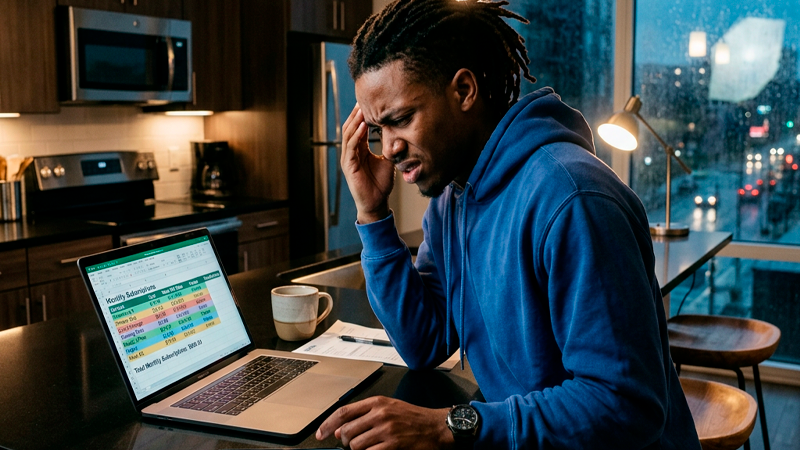

A streaming platform might feel like “just $12.” A cloud storage service feels small. A premium app feels harmless. Add music, fitness apps, delivery memberships, gaming subscriptions, AI tools, software plans, security apps, and random free trials that converted into paid plans, and the number changes fast.

A recent budgeting exercise I helped a friend do became surprisingly ugly.

He believed he spent around $90 per month on recurring services.

The actual number was $312 every month.

That included:

- 4 streaming services

- 2 gaming memberships

- 3 AI tools

- cloud storage

- fitness apps

- meal delivery discounts

- software renewals

- duplicate music subscriptions

The biggest issue was not even the amount itself. It was the fact that almost half of the subscriptions were barely being used.

This happens constantly because companies design subscription models to survive inactivity. They do not need daily engagement. They only need people to forget cancellation exists.

Cheap Monthly Payments Create False Financial Comfort

A $9.99 charge rarely feels dangerous.

A $14.99 renewal does not trigger panic.

Even $25 per month can feel manageable.

But multiple “small” subscriptions combine into something much larger because the brain evaluates them individually instead of collectively. People mentally separate subscriptions instead of treating them as one category.

That changes spending behavior dramatically.

Someone who would never spend $280 at once might comfortably approve fifteen smaller recurring charges without hesitation.

There is another layer many people ignore.

Subscriptions reduce flexibility during financial emergencies.

A person earning good money can still feel financially trapped because recurring payments already consumed part of next month’s income before the paycheck even arrived. That creates a dangerous cycle where income looks higher on paper than it actually feels in daily life.

Annual Plans Sometimes Waste More Money Than Monthly Plans

A lot of finance advice pushes annual subscriptions as the “smart” option because they offer discounts.

Sometimes that works.

Sometimes it quietly locks people into services they stop using after two months.

This is especially common with fitness apps, productivity platforms, language-learning programs, and business software.

A person sees:

- $19 monthly

- or $149 annually

The annual plan feels financially responsible because it “saves money.”

But if the service gets abandoned after 60 days, the cheaper monthly option would have cost far less overall.

That is why cancellation behavior matters more than discount percentages.

One useful rule is surprisingly simple:

Never buy an annual subscription for a habit you have not maintained consistently for at least 90 days.

That single decision can save hundreds of dollars every year.

A lot of unused subscriptions come from optimism purchases rather than actual routines.

Free Trials Cause More Budget Damage Than People Expect

Free trials are dangerous because they bypass normal spending resistance.

Nobody feels stress entering a card for “7 free days.”

But companies know something important about human behavior. Most people do not cancel services immediately after testing them. They postpone the decision.

Then life gets busy.

Then the billing cycle starts.

One of the least obvious money traps happens when free trials begin stacking together across different dates. People lose track of renewal timing completely.

That creates random budget hits throughout the month.

A streaming platform renews on the 4th.

An AI tool renews on the 11th.

A design app renews on the 17th.

A cloud service renews on the 28th.

Individually, the charges feel manageable. Together, they slowly pressure checking accounts and increase reliance on credit cards.

One practical strategy works surprisingly well:

Use a separate debit card with limited balance only for free trials and subscriptions.

That creates visibility instantly. It also prevents forgotten subscriptions from draining primary accounts unexpectedly.

Subscription Inflation Became a Serious Financial Problem

Many subscriptions quietly increase pricing over time.

Not dramatically.

Just enough that people rarely react.

A streaming service increases from $9.99 to $11.99. Then later to $14.99. Then introduces premium tiers. Music platforms, software tools, and cloud services have followed the same pattern repeatedly.

The problem is that people often compare the current price to the last increase instead of the original cost.

Over several years, subscription inflation becomes massive.

A household paying:

- $8 for streaming

- $10 for music

- $15 for software

five years ago may now pay closer to:

- $18 for streaming

- $14 for music

- $30 for software

without consciously deciding to upgrade their lifestyle.

That creates a silent form of lifestyle inflation most budgeting advice barely discusses.

The scary part is that recurring payments scale automatically while salaries often do not.

One Monthly Audit Can Change Spending Fast

People usually imagine budgeting requires spreadsheets, complicated tracking apps, or daily monitoring.

In reality, one simple monthly audit catches most waste quickly.

Open bank statements and look only for recurring charges.

Nothing else.

Do not focus on groceries, gas, or restaurants initially. Just subscriptions.

Then ask three questions:

- Did I use this last month?

- Would I buy this again today?

- Does this save me time, make me money, or improve my life enough to justify the cost?

If the answer becomes unclear, the subscription is probably already failing its purpose.

One overlooked insight is that unused subscriptions also create mental clutter. People carry digital obligations the same way they carry physical clutter in a crowded room.

Canceling unnecessary services often improves financial awareness faster than trying to cut occasional spending like coffee or takeout.

That is why subscription audits produce surprisingly immediate results.

Convenience Can Become Expensive Very Quietly

Many modern services are designed around reducing friction.

Automatic delivery.

Automatic renewals.

Automatic upgrades.

Automatic cloud backups.

Automatic premium access.

Convenience feels efficient, but convenience without active evaluation becomes expensive over time. Companies profit heavily from passive customers who stop reviewing their monthly expenses.

That does not mean subscriptions are bad.

Some subscriptions genuinely save money or improve quality of life. A software platform that generates income, a fitness app used daily, or cloud storage protecting important work can absolutely justify recurring costs.

The real danger starts when subscriptions become invisible.

Once spending becomes invisible, financial control usually weakens faster than people realize. And unlike one-time purchases, recurring payments continue extracting money every single month whether someone actively values the service or not.