Financing Phones Too Often Can Quietly Drain Your Budget

A lot of consumers think monthly payments make expensive phones easier to afford.

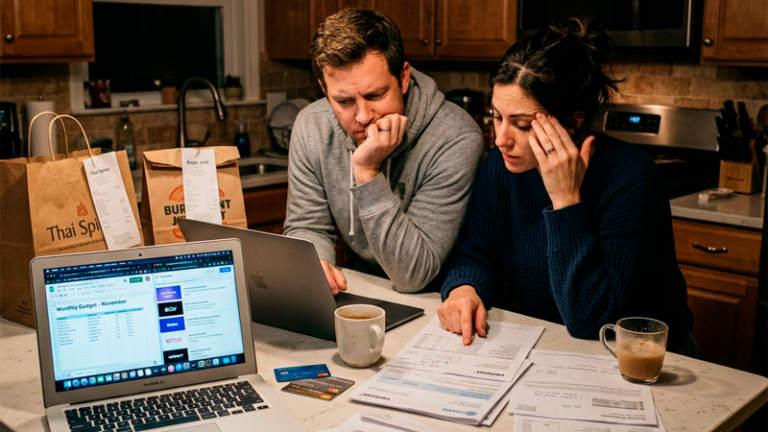

That idea sounds harmless at first. Someone walks into a carrier store planning to buy a normal device, then sees the newest flagship model advertised for “only” $38 per month. The payment feels small enough that upgrading suddenly seems reasonable.

Three years later, many of those same people have almost nothing saved, multiple subscriptions attached to their phone bill, and a habit of replacing devices before they even finish paying them off.

The problem is not the phone itself. The problem is how small monthly payments quietly distort spending decisions.

This happens constantly because modern financing hides the real purchase price extremely well.

Monthly payments reduce the psychological weight of expensive purchases

Most people react differently to $1,400 upfront than they do to $39 per month.

Even though the total cost may be nearly identical, the smaller number feels emotionally manageable. Retailers understand this perfectly. That is why smartphone marketing focuses heavily on monthly pricing instead of full device costs.

A customer comparing phones may think:

- $39 per month feels fine

- $52 per month still seems acceptable

- $61 per month feels “only slightly higher”

But those differences become massive over time.

A person financing a $1,500 phone over 36 months may also add:

- Insurance plans

- Cloud storage upgrades

- Accessory bundles

- Premium carrier packages

Suddenly the phone setup costs $85 to $120 every month without feeling extreme because everything was separated into smaller charges.

That is how relatively normal consumers end up spending luxury-level money on devices they mainly use for social media, streaming, and messaging.

Carrier trade-in programs encourage constant upgrading

One of the smartest strategies used by phone companies involves upgrade cycles.

Many consumers no longer think about fully owning their phones. Instead, they stay trapped inside permanent payment loops where upgrading becomes automatic every one or two years.

The marketing sounds attractive:

- “Upgrade early”

- “Trade in anytime”

- “Get the newest model now”

- “No upfront payment”

What often goes unnoticed is that people remain continuously attached to financing agreements.

Some consumers have paid phone bills for ten straight years without ever experiencing a single month without device payments.

That creates a strange financial effect where expensive technology becomes normalized permanently.

A person who upgrades every two years may spend:

- $12,000 to $18,000 across a decade

- Additional taxes and activation fees

- Repeated accessory purchases

- Ongoing insurance payments

Meanwhile, someone keeping devices longer might spend less than half that amount while barely changing their daily experience.

Most people barely use flagship phone features

This part surprises many buyers after they think honestly about usage habits.

Modern premium smartphones are incredibly powerful, but a huge percentage of users never push those devices anywhere near their limits.

A person may spend $1,300 on a phone capable of:

- Advanced 4K video production

- Console-level gaming

- Professional photography workflows

- Heavy multitasking

- AI processing tools

Then spend most of the day using:

- Messaging apps

- TikTok

- YouTube

- Web browsing

For many users, a well-maintained mid-range phone would perform almost identically during normal daily tasks.

The difference between a $500 phone and a $1,400 phone often matters less after the first few weeks. People adapt quickly to upgraded screens and cameras, which reduces the emotional value much faster than expected.

That adaptation cycle is one reason consumers keep chasing newer models repeatedly.

Cheap financing can damage larger financial goals

Small recurring payments rarely stay isolated.

Someone financing a premium phone may also finance:

- Furniture

- Watches

- Laptops

- Headphones

- TVs

- Cars

Individually, each payment feels manageable.

Combined together, they slowly reduce flexibility everywhere else.

A person spending an extra $70 monthly on premium phone financing and related upgrades could redirect that money toward:

- Emergency savings

- Credit card debt reduction

- Investments

- Car maintenance

- Travel

- Retirement contributions

Over five years, that difference becomes meaningful.

A monthly phone payment is not just a technology expense. It is money permanently unavailable for everything else.

One overlooked issue is how recurring payments reduce risk tolerance. People living with heavy monthly obligations often feel trapped inside jobs or situations they dislike because their financial baseline keeps growing.

That pressure rarely starts with one giant decision. It usually builds through dozens of smaller financing habits.

Repair culture disappeared when financing became normal

Years ago, people commonly repaired phones and kept them longer.

Now many consumers replace devices immediately after relatively minor issues because financing made replacement feel easier than repair.

A cracked screen on a fully owned phone might cost $250 to fix. That sounds expensive upfront, but replacing the entire device through financing often costs far more long-term.

Some consumers effectively restart multi-year payment cycles simply because:

- Battery life dropped

- Camera quality feels outdated

- Storage became full

- Cosmetic damage appeared

- A new color launched

Manufacturers benefit heavily from this behavior because constant upgrading increases long-term revenue dramatically.

At the same time, buyers slowly lose the habit of maximizing the lifespan of expensive products.

Keeping phones longer quietly creates financial advantages

There is an interesting pattern among people who build strong financial stability over time.

Many of them keep electronics longer than expected.

Not because they cannot afford upgrades, but because they understand something important: avoiding unnecessary recurring expenses creates breathing room that compounds quietly for years.

A person keeping a phone for five years instead of upgrading every two years may avoid thousands in unnecessary spending without feeling deprived daily.

That extra margin can absorb emergencies more easily.

It can reduce financial stress.

It can create investment opportunities.

Ironically, some high-income people deliberately use older devices longer because they prioritize flexibility over status signaling.

That mindset tends to grow stronger after people experience how quickly technology loses novelty.

The smartest phone purchase often feels slightly boring

A lot of people expect smart financial decisions to feel exciting.

Usually they do not.

The financially healthier choice is often the less emotional one:

- Buying slightly below budget

- Keeping devices longer

- Ignoring annual upgrade pressure

- Repairing instead of replacing

- Avoiding unnecessary premium plans

Those decisions rarely generate social attention.

But they create something more useful over time.

People who normalize constant device financing often underestimate how many future financial choices become harder because of small monthly obligations that never disappear.