Middle Income Americans Are Quietly Paying Luxury Prices For Everyday Life

A strange financial pattern has been spreading across the United States over the last few years, especially among middle income households trying to maintain a “normal” lifestyle.

People are not necessarily buying mansions.

They are not flying private jets.

Most are not even making reckless financial decisions intentionally.

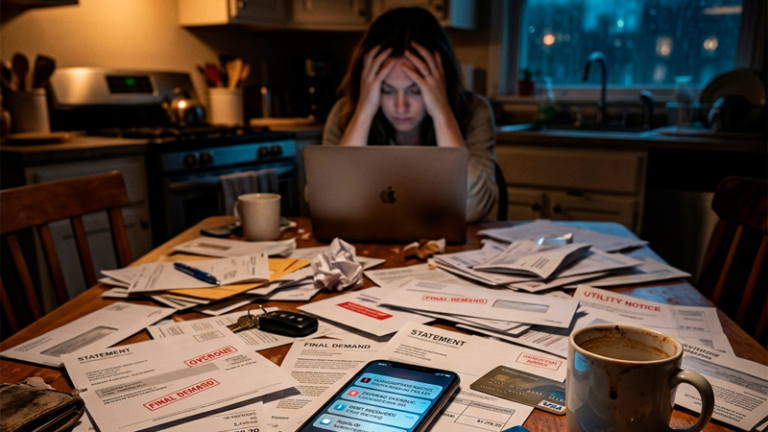

Yet a growing number of families earning between $80,000 and $160,000 per year constantly feel financially cornered by ordinary monthly expenses that used to feel manageable.

What changed is not only inflation.

It is the silent transformation of everyday costs into premium-priced habits.

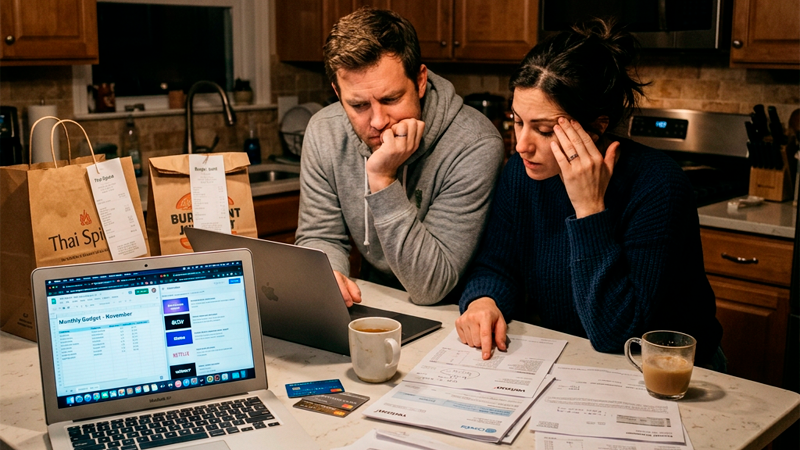

A basic grocery run now feels noticeably heavier on the budget. Casual restaurant visits regularly cross $80 to $120 for families. Even quick convenience purchases slowly pile into surprisingly expensive monthly totals. Many households are spending far more money than they realize simply trying to preserve routines that once felt financially harmless.

A lifestyle that looked comfortably middle class ten years ago now often carries upper-middle-class costs.

And many people only notice the damage after the pressure becomes impossible to ignore.

Monthly Convenience Habits Started Functioning Like Hidden Bills

One major financial problem affecting middle income households today is the normalization of recurring convenience spending.

A lot of purchases no longer feel like spending because they happen automatically.

Streaming services renew silently. Delivery apps save payment information permanently. Subscription trials quietly become recurring charges. Small digital transactions blend into everyday life so smoothly that people stop emotionally registering them as real expenses.

That creates dangerous financial blindness over time.

A household paying for five streaming platforms, multiple cloud subscriptions, premium delivery memberships, music apps, gaming subscriptions, and same-day shipping services can easily lose $400 to $900 monthly without noticing how fragmented the spending became.

The psychological effect matters more than most people realize.

When purchases happen invisibly, consumers naturally spend more aggressively.

Years ago, spending required more friction. People physically handled money, manually entered card information, or actively reviewed purchases more carefully. Today, spending often happens with one click while distracted.

Small recurring charges became one of the easiest ways for households to quietly lose thousands of dollars every year.

Many families underestimate their monthly leakage because no single purchase feels catastrophic individually.

And unfortunately, companies increasingly design services around that exact behavior pattern.

Food Delivery Quietly Became A Massive Financial Drain

One overlooked money shift involves how aggressively food delivery transformed household spending habits.

A simple dinner that originally costs $18 or $20 can quickly become $35 or more after taxes, delivery fees, service charges, inflated menu pricing, and tips.

For people ordering multiple times weekly, the math becomes brutal surprisingly fast.

A family using delivery apps four nights per week may spend an additional $400 to $700 monthly compared to preparing similar meals at home.

That difference alone can exceed:

- a car payment

- emergency savings contributions

- retirement deposits

- utility bills

- insurance costs

The dangerous part is emotional normalization.

People no longer view delivery as an occasional convenience.

For many households, it became routine.

Busy schedules, remote work exhaustion, long commutes, and digital convenience culture all contributed to this behavioral shift. Cooking started feeling like extra labor instead of normal daily activity.

What once felt like an occasional luxury quietly evolved into a permanent budget category.

And recurring convenience spending usually grows faster than income over time.

This pattern appears heavily among younger professionals living in expensive cities where long work hours already create constant mental fatigue.

The Pressure To Look Financially Stable Became Expensive

Another major issue affecting middle income households is social comparison pressure.

Modern consumers no longer compare themselves only to neighbors or coworkers. They compare themselves against curated online lifestyles constantly throughout the day.

That changes spending behavior dramatically.

People feel pressure to maintain appearances even when finances privately feel unstable underneath.

A newer SUV feels emotionally necessary because “everyone else” appears upgraded online. Expensive apartments suddenly feel justified because social media normalizes luxury interiors constantly. Vacation financing starts feeling acceptable because endless travel content creates the illusion that frequent trips are standard adult behavior.

This creates subtle but dangerous financial distortion.

Consumers begin making emotional spending decisions disguised as practical upgrades.

A person earning a solid salary may still carry constant financial stress because lifestyle expectations expanded faster than income itself.

Many households are not drowning because of one terrible decision.

They are drowning slowly through dozens of socially normalized upgrades happening simultaneously.

And once those upgrades become emotionally attached to identity, reducing spending feels psychologically painful even when finances clearly require it.

That is why many middle income earners appear financially successful while secretly operating with almost no flexibility month to month.

Monthly Payments Changed The Way Americans Evaluate Purchases

One of the biggest financial traps today is the obsession with monthly affordability instead of total cost.

Many consumers no longer ask:

“Can I truly afford this?”

They ask:

“Can I survive this monthly payment?”

That mindset shift changed spending culture completely.

Cars became longer-term financing contracts. Phones became permanent upgrade cycles. Furniture, electronics, vacations, gym equipment, and even groceries increasingly moved into installment-based spending systems.

A purchase that sounds manageable at $89 monthly often feels emotionally harmless.

But five separate payments of $89 create a completely different financial reality.

The modern economy increasingly encourages consumers to divide large purchases into smaller emotional pieces because smaller numbers reduce spending resistance psychologically.

Unfortunately, long-term financial pressure compounds quietly underneath.

Many Americans now carry:

- multiple installment plans

- financed electronics

- rolling credit card balances

- vehicle payments extending beyond 72 months

- subscription ecosystems stacked together

At first, each payment feels manageable individually.

Collectively, they create permanent pressure.

The danger is not always overspending recklessly.

The danger is building a lifestyle where nearly every future paycheck already has obligations attached before it even arrives.

That situation leaves households extremely vulnerable to inflation, layoffs, emergencies, or unexpected repairs.

Some Financially Stable Families Actually Look Less Impressive Online

One surprising reality about financially stable households is that they often appear less flashy than heavily leveraged households.

People building real long-term stability usually avoid excessive recurring obligations.

They keep cars longer.

They delay unnecessary upgrades.

They resist lifestyle inflation after promotions or salary increases.

And most importantly, they intentionally leave breathing room inside the budget.

That flexibility matters enormously during economic uncertainty.

A household spending 95% of monthly income may appear wealthier externally than a family spending 65%, but the second household often has dramatically stronger long-term security.

Emergency repairs become manageable instead of devastating.

Medical bills create stress instead of panic.

Temporary income disruptions become survivable instead of catastrophic.

Unfortunately, restraint rarely looks impressive online.

Social media rewards visible consumption far more than quiet financial discipline.

That distortion causes many people to underestimate the value of stability until financial pressure becomes overwhelming personally.

Financial peace usually looks far less glamorous than social media suggests.

But long-term stability often comes from lowering obligations, not increasing appearances.

More middle income households are beginning to recognize that reality after years of financial exhaustion caused by constant lifestyle pressure.

A Quiet Financial Reset Is Already Starting

Across the country, many consumers are slowly changing their habits again.

People are cooking at home more frequently. Subscription cancellations increased noticeably over the last few years. Used vehicles regained popularity. Some younger adults are actively rejecting constant upgrade culture altogether.

Part of this shift comes from inflation fatigue.

Part comes from economic uncertainty.

But another major reason is emotional burnout from constantly trying to maintain expensive routines that no longer feel worth the financial pressure attached to them.

Consumers are beginning to question purchases that previously felt automatic.

Do they actually need constant delivery?

Do they really need annual phone upgrades?

Does every convenience justify another recurring charge?

That mindset shift matters because awareness is usually the first stage of stronger financial behavior.

Most households do not collapse financially because of one massive mistake.

More often, they slowly absorb hundreds of smaller financial obligations until flexibility disappears completely.

And once people recognize how much invisible spending controls their budget, priorities often begin changing naturally.

Not overnight.

But gradually.

FAQ

Why do middle income families still feel financially stressed despite decent salaries?

Many households face rising housing costs, recurring subscription spending, delivery expenses, financing payments, and lifestyle inflation simultaneously. Even strong incomes can feel tight when recurring obligations consume most monthly cash flow.

What is lifestyle inflation?

Lifestyle inflation happens when spending increases alongside income growth. People often upgrade cars, housing, travel habits, electronics, and subscriptions after raises or promotions, reducing the long-term financial benefit of earning more money.

Are subscriptions really a major financial problem?

Yes, especially when multiple services stack together over time. Streaming platforms, premium memberships, cloud storage, delivery services, and financed purchases can quietly create hundreds of dollars in recurring monthly expenses.

What financial habit helps reduce long term money pressure?

Maintaining lower recurring obligations is one of the strongest ways to improve long-term stability. Households with fewer monthly payments usually handle emergencies and economic changes far more comfortably.