The Growing Financial Risks Behind Buy Now Pay Later Apps

A lot of people still think Buy Now Pay Later apps are safer than credit cards.

That assumption helped these services explode across online shopping, clothing stores, electronics retailers, furniture websites, travel bookings, and even grocery apps. Splitting a $240 purchase into four smaller payments feels harmless compared to carrying a revolving balance on a traditional credit card.

But many consumers are discovering a different reality after months of stacking multiple payment plans at the same time.

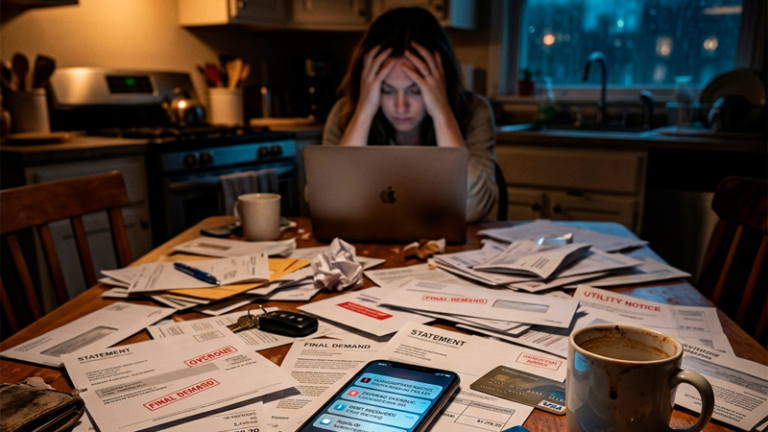

The problem is not usually one purchase. It is the accumulation.

A person using three or four installment apps simultaneously can end up managing 12 to 20 separate automatic withdrawals every month without fully realizing how much future income is already committed.

Small payments create a false sense of affordability

Most Buy Now Pay Later services are designed around psychology more than mathematics.

A $900 laptop sounds expensive. Four payments of $225 sound manageable.

Retailers understand that consumers spend more when purchases feel broken into smaller pieces. Several studies inside retail marketing have shown shoppers are more likely to upgrade products, add accessories, or complete impulse purchases when the upfront pain feels reduced.

That changes buying behavior fast.

Someone originally planning to spend $80 on shoes suddenly justifies spending $170 because the checkout screen says “only $42 today.”

The dangerous part is that future income starts getting spent before it even arrives.

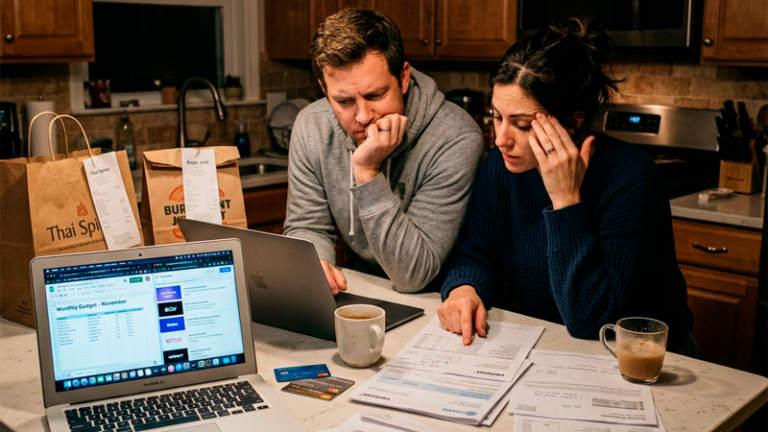

By itself, one installment plan may not create major financial stress. But layered across clothing, streaming equipment, beauty products, electronics, furniture, and travel bookings, the monthly obligations quietly multiply.

Many users do not notice the pressure until:

- bank balances start shrinking unexpectedly

- overdraft fees appear

- payday timing becomes stressful

- minimum savings disappear

- late fees begin stacking together

The payment structure hides the full picture remarkably well.

Late fees hit lower-income users hardest

One overlooked reality is that Buy Now Pay Later penalties often impact people already operating with tight cash flow.

Missing a $60 payment may not sound catastrophic, but consequences build quickly:

- late fees

- overdraft charges

- account restrictions

- collection activity

- credit reporting in some cases

A consumer juggling multiple installment plans can suddenly face five or six payment due dates inside a single week.

That becomes risky when income arrives inconsistently.

Freelancers, rideshare drivers, restaurant workers, commission-based employees, and hourly workers are especially vulnerable because their monthly cash flow may fluctuate dramatically. One slow week can create a chain reaction across multiple automatic payments.

Some users end up taking new installment plans simply to preserve cash temporarily from older obligations.

That cycle starts resembling debt dependency far faster than people expect.

Retailers love installment apps for a reason

These payment systems increase spending behavior very effectively.

Online retailers regularly report:

- higher average order values

- fewer abandoned carts

- larger impulse purchases

- increased mobile conversion rates

That is why Buy Now Pay Later options now appear almost everywhere.

The average shopper interprets installment offers as financial flexibility. Retailers often see them as sales acceleration tools.

There is a subtle but important difference between:

- using installments strategically

- using installments to bypass affordability limits

A consumer carefully splitting a planned appliance purchase with zero fees is very different from someone financing routine shopping every month because checking account balances remain tight.

The second situation creates long-term pressure that rarely shows up immediately.

The credit score impact is becoming more complicated

A few years ago, many installment apps operated mostly outside traditional credit systems.

That landscape is changing.

Some providers now:

- report missed payments

- run soft credit checks

- share repayment behavior with credit bureaus

- tighten approval algorithms

Consumers assuming these services are “invisible debt” may eventually discover otherwise.

One missed payment may not destroy a credit score overnight, but patterns matter. Multiple missed installment plans across different providers can create broader financial instability signals over time.

There is also a less obvious risk.

Frequent installment usage can distort a person’s perception of what they can truly afford monthly. Someone with $2,300 in monthly income may unknowingly commit $1,100 of future paychecks through scattered automatic withdrawals before rent, insurance, fuel, or groceries even enter the equation.

That financial compression becomes dangerous quickly.

Subscription culture made the problem worse

Ten years ago, consumers mostly managed:

- rent

- utilities

- one or two credit cards

- maybe a car payment

Now monthly financial life looks completely different.

People often juggle:

- streaming services

- app subscriptions

- cloud storage

- gym memberships

- financing plans

- digital memberships

- installment purchases

- recurring delivery services

Buy Now Pay Later apps entered an environment where automatic billing already dominates personal finance.

That creates a hidden issue many people underestimate.

Modern consumers are no longer actively choosing every expense each month. A growing percentage of money disappears automatically before conscious spending decisions even happen.

That psychological separation reduces spending awareness significantly.

Zero interest does not always mean zero cost

A lot of installment promotions advertise zero interest financing.

Technically, many do offer true zero-interest structures if payments are completed exactly on time. But consumers still absorb indirect costs through behavioral spending changes.

One financial counselor explained it simply.

People tend to ask:

- “Can I afford this payment?”

instead of: - “Should I spend this money at all?”

That mindset shift matters enormously.

A person who would hesitate before spending $1,400 cash on furniture may instantly approve the purchase once it becomes “just $116 monthly.”

The installment structure changes emotional resistance.

That is one reason many consumers using these services report owning more products while simultaneously feeling financially tighter than before.

More convenience does not automatically create more financial stability.

Emergency savings are often the first casualty

One practical pattern appears repeatedly among heavy installment users.

Emergency savings start disappearing.

When too much future income becomes pre-allocated to payments, consumers lose flexibility. Unexpected expenses like:

- car repairs

- medical bills

- rent increases

- pet emergencies

- travel needs

suddenly become difficult to absorb without new debt.

This creates a dangerous financial contradiction.

Many installment users believe they are avoiding traditional debt while gradually reducing the exact cash reserves that protect people from financial emergencies.

A person with no credit card balance but only $140 in savings is still financially fragile.

That distinction gets ignored surprisingly often online.

Installment apps work best when used rarely

Buy Now Pay Later services are not automatically harmful.

Used carefully, they can help consumers:

- preserve short-term liquidity

- avoid high-interest credit cards

- manage planned large purchases

- spread predictable costs responsibly

But frequency changes everything.

Once installment payments become part of normal monthly lifestyle spending instead of occasional planned financing, financial pressure tends to increase quietly in the background.

That is what catches many people off guard.

The danger usually does not arrive through one catastrophic purchase. It arrives through dozens of smaller decisions that individually feel reasonable until the combined payment load starts controlling future income before it even reaches the bank account.